The urgency of the company response to climate change is more important now than ever before. The recent findings from the UN’s Intergovernmental Panel on Climate Change (IPCC) highlighted the need for urgent action on greenhouse gases, and once again put heavy-emitting sectors under the spotlight.

The oil & gas industry is amongst the most emissions intensive, with the production and use of oil & gas accounting for over half of global greenhouse gas emissions associated with energy consumption. This equates to more than 17 billion tonnes of carbon dioxide equivalent every year.

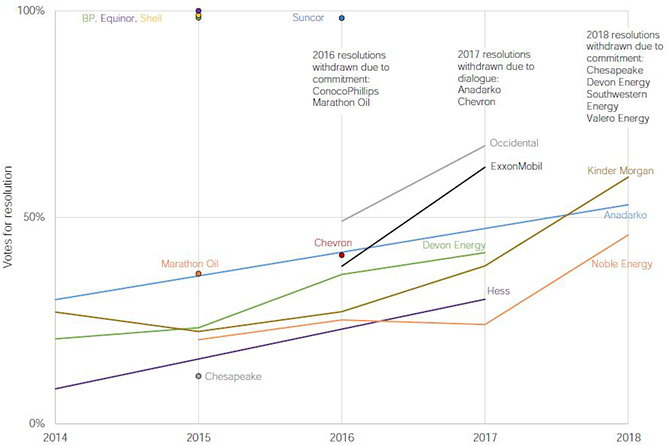

The rise of shareholder climate resolutions

It is therefore positive to see that shareholder resolutions addressing climate issues are winning growing support. Our analysis has shown investors are putting increasing pressure on oil & gas companies, with the number of climate shareholder resolutions filed more than doubling in the last five years compared to the five years prior.

We have seen several historic milestones, most notably the votes in 2017 at ExxonMobil and Occidental, where a majority of shareholders (including the two largest fund managers, BlackRock and Vanguard) voted against management recommendations and in favour of more climate risk disclosure.

This is part of a growing trend of increasing investor scrutiny on climate change across the industry. Resolutions calling for companies to report on portfolio resilience and 2-degree analysis are gaining an increasing share of the vote (see Figure 1).

Figure 1: Votes for resolutions relating to ‘reporting on 2-degree analysis and strategy’

Votes for these resolutions have grown from an average of 21% in 2014 to 53% in 2018 (a compound annual growth rate of 26%). Source: CDP, company reports, Ceres

Investor initiatives addressing climate change are scaling up, as illustrated by the Investor Agenda and Climate Action 100+.

Today, all eyes were on BP’s AGM, where shareholders voted on two climate-related resolutions. The first, filed by Climate Action 100+, called for the company to describe how its strategy is consistent with the goals of the Paris Agreement.

This resolution was supported by BP, and it received a 99.14% majority vote. However, the resolution did not go as far as the recent joint statement by Climate Action 100+ and Shell, in which Shell looks to operationalise its long-term net carbon footprint ambition by setting shorter-term targets over three to five-year periods.

The second resolution, filed by activist investor group Follow This, requested BP to set firm targets to meet the Paris goals. Although not supported by company management, and despite the vote only achieving a 8.35% motion in favour, this was more than was achieved by a similar resolution at Shell’s AGM last year.

These resolutions send a further signal to other companies – a growing number of investors are looking for oil & gas companies to demonstrate their ability to adapt to the energy transition and evidence that strategies are being adopted to ensure resilience for the changes ahead.

Beyond the Cycle

Our report “Beyond the Cycle” examined how 24 of the world’s largest publicly listed oil & gas companies, together making up around a third of global production, are preparing for a low-carbon transition.

The analysis showed that 15 of the 24 oil & gas companies have now set climate targets, with Repsol, Shell and Total the most ambitious.

European oil & gas majors including BP, Eni, Equinor, Total and Shell are investing the most in low carbon - however the industry’s spend as a whole remains relatively low at only 1.3% of total capital expenditure (CAPEX) in 2018.

The landmark Paris Agreement set the direction of travel and last year’s report from the IPCC drew a line in the sand.

We must drastically decrease our global dependence on fossil fuels or we cause irreversible damage to the planet. For the oil & gas industry, which still needs major transformation, the pressure is rising.