New CDP report reveals miners such as Anglo American and Vedanta Resources at risk

- Mining companies generate US$16 billion in emissions costs in their value chain from a low carbon price of $7/tonne CO2;

- Miners are exposed to up to 30 times more emissions by passing the buck down their value chains, equivalent to India’s entire annual CO2 emissions;

- Major mining companies remain heavily dependent on the sale and use of fossil fuels;

- China could disrupt the commodities market through introduction of its carbon pricing scheme;

- A quarter of mining production, representing up to US$50bn in annual revenue, could be exposed to water shortages and drought by 2030;

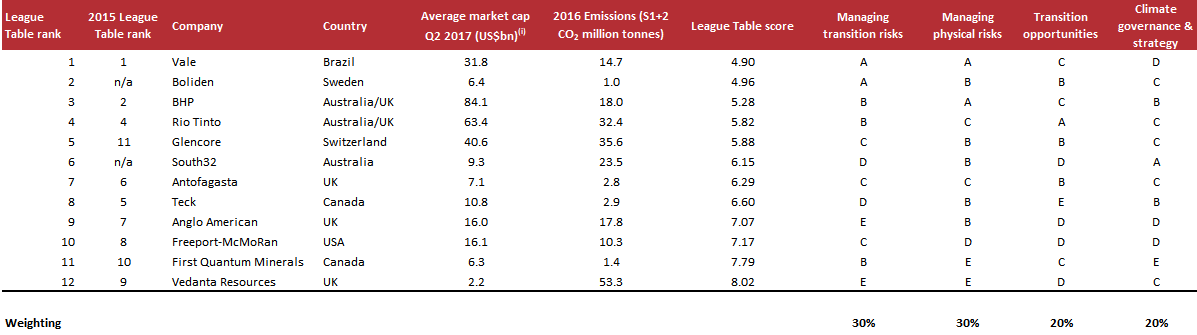

- Vale, Boliden and BHP are best performing companies on carbon-related metrics relative to peers; Vedanta Resources, First Quantum Minerals and Freeport McMoRan rank lowest of companies assessed.

July 20, 2017: A new report ‘Digging Deep’ analyzing a US$294 billion market cap grouping of the world’s major publicly-listed mining companies reveals they are generating up to US$16 billion in emissions costs by passing down the risk in their value chain[1]. Miners are exposed to up to 30 times more emissions, equivalent to India's annual emissions[2], by passing the buck down despite efforts to reduce them in the last six years.

The report from CDP – voted no. 1 climate change research provider by institutional investors – reveals mining companies remain heavily dependent on fossil fuels despite some sourcing almost half of their energy consumption from renewables. Miners are also spending almost half of their capital expenditure on low-carbon materials, such as copper and nickel, yet continue to spend over a quarter on fossil fuels.

Paul Simpson, CEO of CDP, said: “The mining sector must take stock and not risk being left behind in the global transition towards a low-carbon economy. Miners depend on continuing demand for the commodities they supply and the countries consuming the most commodities are making significant changes in addressing climate change. This is most acute in China’s proposal of putting a price on carbon, signifying a strong transition to a low-carbon economy. The recent recommendations of Mark Carney’s Taskforce on Climate-related Financial Disclosure (TCFD) is another factor of increasing investor pressure for companies to not only disclose but manage their transition risk."

There are signs of strategic moves away from thermal coal across the 12 companies, yet this is offset by twice as much oil and gas production over the last six years. Rio Tinto for example is divesting from thermal coal leaving their portfolio better positioned in terms of low-carbon resilience, yet Glencore is bucking this trend as evident in their recent rejected bid for Rio Tinto’s coal assets despite global coal consumption falling for second year in a row[3].

As the mining sector is heavily dependent on continuing demand for their supply of commodities, it has the potential to be hit hard by China’s proposals for pricing carbon. China’s scheme could be a catalyst for more widespread carbon pricing in commodity consuming countries, disrupting commodities markets and demand for miners’ output. Carbon pricing has already been introduced in mining countries such as Chile earlier this year and it is due to go live in South Africa and Canada in 2018.

The research also finds a quarter of mining production, representing up to US$50 billion in annual revenue, will be exposed to significant water stress such as drought and shortages by 2030[4]. Major mining regions such as Chile, Australia and South Africa are likely to be the most adversely affected.

Today’s report benchmarks major miners’ performance on climate issues and finds that Vale, Boliden and BHP are the best performing companies on carbon-related metrics relative to peers in the report sample, with Freeport-McMoRan, First Quantum Minerals and Vedanta Resources ranking lowest among those who disclose to CDP.

CDP’s summary League Table for mining companies is below:

Tarek Soliman, Senior Analyst, Investor Research at CDP said: “As a sector with a significant carbon footprint and that supplies the wider economy, mining is faced with the reality that a low-carbon transition will impact many of the industries that currently demand its commodities. Accordingly, the companies we featured in our research will need to adjust their long-term strategies to reflect the changing grounds in carbon regulation and commodity consumption trends in light of events such as China’s proposed carbon pricing scheme. Miners in general have cut operational emissions and costs in recent years as well as scaling down thermal coal exposure, however their significant Scope 3 emissions footprints remain a concern. Some companies are doing more than others to ready themselves for a transition, and investors will want to know what the potential implications are for their portfolios.”

Other findings from the report include:

- Looking ahead: Resilience tests through forward-looking climate scenario analysis is yet to become common industry practice. However, investors are increasingly highlighting such analysis as a necessary aspect of companies’ disclosure of planning for a low-carbon transition that would achieve below 2°C of warming as evident in the TCFD and ‘Aiming for A’ initiative.

- Innovation: Disruptive technologies and digital innovations will transform the mining sector. Miners are beginning to focus more attention on innovative technologies which can deliver future productivity gains and sustainable growth.

- Climate policy: InfluenceMap analysis finds miners remain opposed to a number of climate policies, such as the current proposed South African national carbon tax.

- Circular economy: Material recycling and the circular economy could offer a potential medium term secondary source of commodity market supply. Pricing dynamics and market forces play large roles in determining how much this will disrupt mining companies’ production disruption.

- Executive remuneration packages: Although seven companies out of 12 analyzed has specific measures for its CEO based on climate metrics, only up to 5% of total remuneration accounts for climate related compensation.

- Emissions targets: Only one of the companies featured, South32, has a commitment to fully decarbonize by 2050. Nine of the companies have shorter term emissions reduction targets.

You can view the executive summary of the report here.

- ENDS –

Notes to editor

For more information or for exclusive interviews with the CDP team, please contact:

- Caroline Barraclough, ESG Communications t: +447503 771694 | e: [email protected]

- Rojin Kiadeh, CDP t: +44 (0) 203 818 3912 | e: [email protected]

Scope and methodology: Full details of the scope of the report and methodology used are included in the full version of the report which can be accessed by CDP signatories. For the full report please contact [email protected]

About CDP and this report

About CDP

CDP is an international non-profit that drives companies and governments to reduce their greenhouse gas emissions, safeguard water resources and protect forests. Voted number one climate research provider by investors and working with institutional investors with assets of US$100 trillion, we leverage investor and buyer power to motivate companies to disclose and manage their environmental impacts. Over 5,800 companies with some 60% of global market capitalization disclosed environmental data through CDP in 2016. This is in addition to the over 500 cities and 100 states and regions who disclosed, making CDP’s platform one of the richest sources of information globally on how companies and governments are driving environmental change. CDP, formerly Carbon Disclosure Project, is a founding member of the We Mean Business Coalition. Please visit www.cdp.net or follow us @CDP to find out more

The report

This research is part of a series of award winning in-depth sector analysis by CDP to provide investors with the most comprehensive environmental data analysis. It aims to identify the most material metrics for each specific sector and how they link to financial performance. Our methodology is unique as the weighting assigned to each metric is transparent and can be applied individually according to investor preferences. These rankings are not intended to identify definitive winners and losers for investment purposes, but rather to indicate strategic advantage in an industry where there is a significant regulatory impact on all major markets.

Reports on the oil & gas, steel, cement, automotive, electric utilities and chemicals and mining industries were released in 2015 and 2016.

[1] Uses average US$7 carbon price on the companies’ Scope 3 emissions footprint.

[2] Miners’ value chains contain up to 30 times more carbon than their own operations. These refer to company downstream (Scope 3) emissions. Estimated Scope 3 emissions from the 12 companies in 2016 was 2.36 gigatonnes C02 compared to 225 million C02 tonnes of operational (Scope 1 + 2) emissions. This figure represents India’s direct emissions from Netherlands Environmental Assessment Agency’s CO2 time series 1990-2015 per region/country

[3] BP Statistical Review of World Energy: June 2017

[4] WRI’s Aqueduct tool