Welcome to CDP's global website

Please select the site for your country / region to view the most suitable information

CDP 2023 disclosure data factsheet

In 2023, 23,000+ companies - representing a staggering US$67 trillion in market capitalization - disclosed their environmental performance data to CDP. This factsheet presents an overview of the key findings and emerging trends from this data, showcasing CDP's expanding coverage and growth across regions, markets, and the key environmental themes of climate change, forests, water security, biodiversity, and now, plastics.

With the number of companies disclosing environmental information growing annually, CDP's role as an accountability mechanism is strengthened. This factsheet uses the wealth of data that CDP holds to provide transparency and insight into the evolving landscape of environmental disclosures.

Skip to:

Disclosure beyond climate

56% of disclosing companies are providing environmental performance information on nature-related issues beyond climate, indicating a growing recognition that providing disclosure on climate alone is not enough.

Key messages

- In 2023, disclosure numbers rose by 24% from the 18,700+ companies that disclosed through CDP in 2022 – and marked an over 140% increase from disclosure in 2020.

- ~ 8,000 companies started their journey by disclosing for the first time.

- A growing number of companies are providing nature-related disclosures beyond climate, indicating a rise in awareness that companies have impacts and dependencies on nature, with resulting risks and opportunities. While this is positive progress, it needs to be matched by firm action to manage nature-related impacts, risks and opportunities across value chains.

Coverage by region

CDP corporate disclosers are based in approximately 130 countries across the world. Each region has experienced a notable increase in the number of companies disclosing.

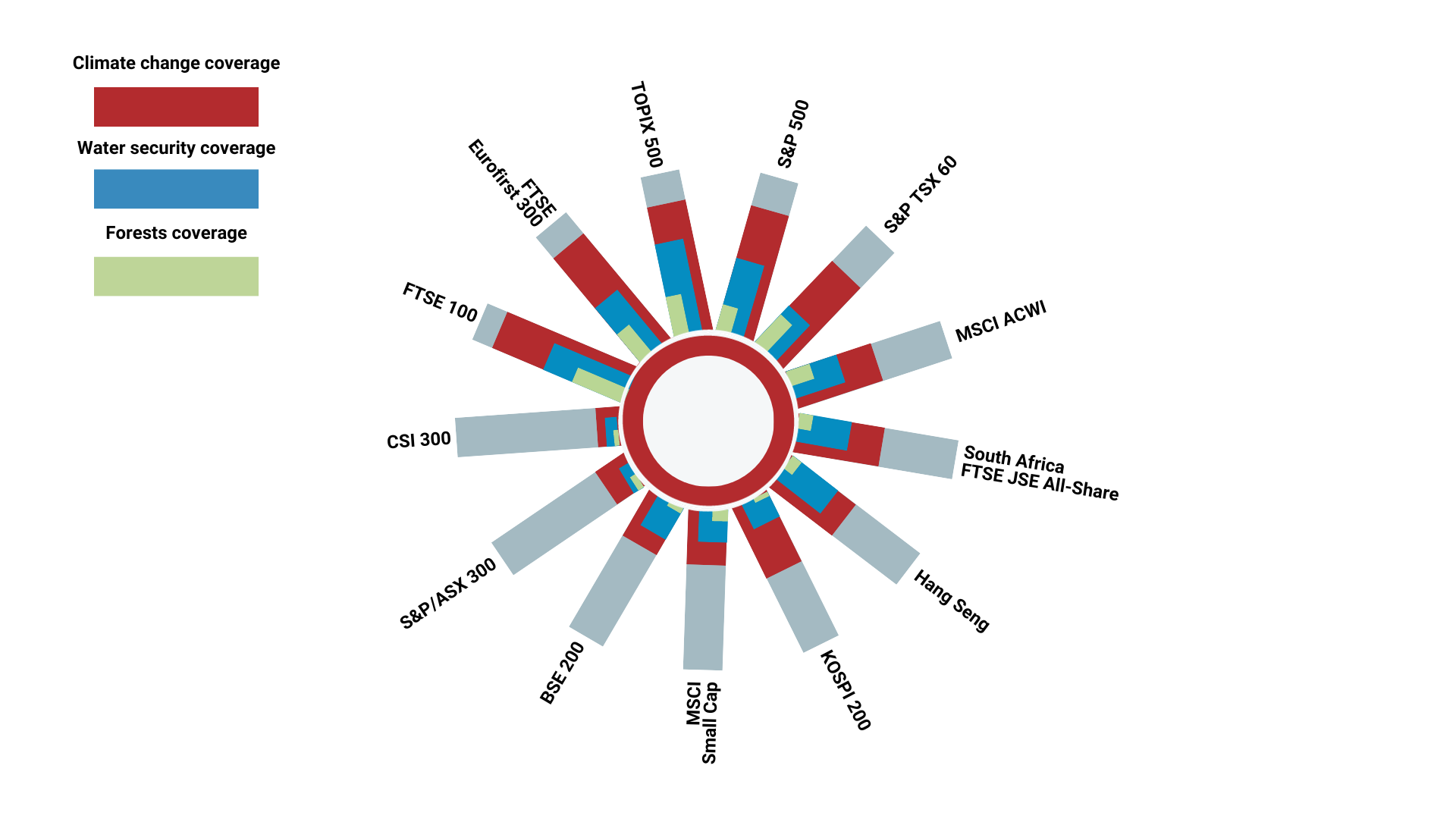

Coverage of indices

Companies in key market indices across the globe are disclosing environmental data to CDP.

| Market Index |

Climate change coverage | Forests coverage | Water security coverage |

| S&P 500 | 86% | 14% | 41% |

| FTSE 100 | 94% | 28% | 43% |

| MSCI ACWI | 61% | 9% | 28% |

| MSCI Small Cap | 40% | 5% | 14% |

| TOPIX 500 | 88% |

15% | 53% |

| FTSE Eurofirst 300 | 91% | 21% | 41% |

| South Africa - FTSE JSE All-Share | 57% | 9% | 30% |

| BSE 200 | 40% |

3% | 21% |

| S&P TSX 60 | 78% | 20% | 30% |

| KOSPI 200 | 54% | 1% | 16% |

| Hang Seng | 54% | 4% | 29% |

| CSI 300 | 18% | 1% | 7% |

| S&P/ASX 300 | 27% |

3% | 7% |

Key messages

- Environmental disclosure is becoming a global market norm, as seen by the increase in disclosures across all regions and the coverage of market indices across developed and emerging markets.

- With many disclosing companies operating in regions anticipating mandatory disclosure, voluntary disclosure through CDP allows them to gain a competitive edge and positions them ahead of the trend.

Water withdrawal reduction

- 30% of all disclosers (1,458 out of 4,815) are setting water withdrawal reduction targets – a dramatic increase from 14.6% in 2022. The number of companies setting targets relating to pollution and the provision of safe water, sanitation and hygiene (WASH) has also increased, indicating a surge in ambition and action in these important areas.

- About half of the 223 companies that have disclosed consistently on water between 2015 and 2023 have reduced their water withdrawals. 70,134 million cubic meters of water have been saved by 120 companies, equivalent to 10 times the size of Loch Ness in Scotland.

Progress on eradicating deforestation from supply chains

Companies are demonstrating progress on eradicating deforestation from their supply chains.

- About half of the 242 companies (126 companies; 52%) that have disclosed consistently on their management of deforestation between 2020 and 2023 now report that they are close to eradicating deforestation for at least one commodity they source.

- This represents a substantial 40% increase from the number of companies reporting the same in 2020 (90 companies).

- Overall, this still represents only a small group of companies – 35% of all companies disclosing in 2023 claiming to be nearly deforestation-free1 for at least one commodity (189 companies).

The slow rate of action and transition to no-deforestation is leaving companies and financial institutions exposed to risks as a resilient economy cannot be accomplished without progress on deforestation. In 2022, nearly four million hectares of pristine forests were destroyed, releasing 2.5 Gt CO2e – equivalent to the annual fossil fuel emissions of India2.

Emissions disclosure

Key messages

- In the last nine years, reported reductions in water withdrawal volumes have decreased among roughly half of the 223 companies that have disclosed consistently on water during this time.

- While disclosure of emissions is increasingly mainstreamed as seen in a relatively high disclosure rate of Scope 1 and 2 emissions, this is just the start, as only 37% of companies disclosed emissions across all three scopes.

- In the past three years, there has been a substantial increase in the number of companies reporting they are close to eradicating deforestation for at least one commodity (40%; 90 companies). However this still only represents a small group of companies. The rate of action and transition to no-deforestation needs to be accelerated.

CDP's growing number of energy disclosures indicates that companies and financial institutions are embracing the transition to a low-carbon economy and are aiming for transparency. While leading companies are setting targets to enhance their renewable energy consumption, the majority are still lagging behind in quality disclosures.

Disclosure on energy usage

- 56% of the 23,000+ disclosers in 2023 (13,000+) disclosed how much energy they used.

- 31% of these companies (4,030) disclosed having no energy consumption from renewable sources.

Disclosure on renewable energy targets

- Only 10% of all disclosing organizations (2,229) have set renewable energy consumption targets.

- About two-thirds of these organizations disclosed that they aim for 90-100% renewable energy consumption. Of these, 70% have a target date of 2030 or earlier.

Renewable energy, deforestation and biodiversity

While the transition to 100% renewable energy use is crucial to mitigate climate change, the source of renewable energy used matters.

- Some forms of renewable energy could cause more issues than they would solve. For example, biofuel production can be associated with land use changes that can cancel out any emissions benefits as well as having negative impacts on biodiversity and food production.

- The use of the right kind of renewable energy sources needs to be encouraged, otherwise there is a risk of fueling the biodiversity crisis.

The Energy-Water Nexus

- In 2023, 180 companies across the sectors critical to the energy transition – power generation, fossil fuels and metallic mineral mining – disclosed their water risks, impacts and opportunities. However, 637 companies were requested to do so. At 21%, the response rate for companies operating in the fossil fuel sector was staggeringly low, despite the critical impact this sector has on water availability and quantity. Pressures on water availability need to be carefully managed if the world wants to reach zero emissions and adapt to the impacts of extreme weather events.

The good news is that the majority of disclosing companies in these sectors are conducting water-related risk assessments. 80% of companies in the fossil fuel industry did so (compared to 62% across all reporting industries). These assessments are paramount, to enable companies to anticipate and mitigate risks that could have substantive impacts on their operations, as well as surrounding communities and ecosystems.

Financial institution exposure to fossil fuels

- Almost 50% of the 575 financial institutions that disclosed in 2023 report holding an estimated US$9 trillion in fossil fuel financing across their portfolios – equivalent to the combined GDP of Japan and Germany.

Key messages

- Most of the 13,000 companies that disclosed on their energy consumption report that they use renewable energy in their energy mix.

- However, 44% of the overall number of disclosing companies are still not reporting on their energy consumption data. In the transition to a low-carbon economy, stakeholders – including investors – must encourage comprehensive disclosure from all companies to improve transparency and a better understanding of corporate environmental impact and risk exposure.

- Although companies have begun embracing the transition to renewable energy, ambition is still lacking with only 10% of all disclosers setting targets for renewable energy consumption.

- It is important for the renewable energy transition to rely on sources of renewable energy which do not have negative impacts on nature and climate. For example, the use of wood-based biomass can result in an increase in deforestation and worsening of the biodiversity crisis.

- Greater accountability on water impact disclosure is needed from the energy sector. Investors must call for increased transparency from companies in this sector in relation to their high impact on water resources.

- Financial institutions have a significant exposure to carbon-intensive assets across their portfolio. They must take more ambitious steps towards phasing out fossil fuels across their portfolios to meet targets.

Climate-related risks and opportunities

Of the total number of companies that disclosed on climate change:

- 52% of disclosing companies (11,998) reported identifying exposure to inherent climate-related risks that potentially posed substantive financial or strategic impact on their business.

- 63% of disclosing companies (14,707) identified climate-related opportunities with the potential for substantive financial or strategic impact on their business.

Forests-related risks and opportunities

Of the total number of companies that disclosed on forests:

- 65% of disclosing companies (572) identified exposure to inherent forest-related risks that potentially posed substantive financial or strategic impact on their business (for at least one commodity).

- 73% of disclosing companies (647) identified forest-related opportunities with the potential for substantive financial or strategic impact on their business (for at least one commodity).

Water-related risks and opportunities

Of the total number of companies that disclosed on water:

- 44% of disclosing companies (2,096) identified exposure to inherent water-related risks that potentially posed substantial financial or strategic impact on their business.

- 50% of disclosing companies (2,431) identified water-related opportunities with the potential for substantive financial or strategic impact on their business.

Key messages

- Most disclosing companies identified risks and opportunities which potentially posed substantial financial or strategic impact on their business.

- More companies have identified opportunities than risks, across all themes.

- It is less costly for businesses to manage their risks than bear the potential financial impact of these risks materializing, across all themes.

Portfolio emissions targets

In 2023, 575 financial institutions (FIs) disclosed to the Financial Services questionnaire.

- Only 37% reported having set a portfolio target – up from 29% (out of 556 institutions) in 2022.

- Meanwhile, 38% reported targets that only cover their operational emissions.

- 25% did not report any targets at all.

FIs assessing portfolio impacts by theme

Key messages

- An increasing number of FIs are beginning to measure their portfolio impacts across themes. The number of FIs that disclosed measuring their portfolio impact on climate rose from 66% in 2022 to 72% in 2023.

- A significant gap remains in forest and water-related metrics despite this increase in FIs measuring climate-related impact. Only 13% reported that they measure their portfolio impacts on either one or both themes.

- Despite notable improvements since 2022, FIs are still falling short on the scale of action needed for robust portfolio target-setting. There is significant ground to cover. As CDP's 2022 Financial Services Disclosure report shows, although portfolio emissions of global FIs are on average over 750x larger than their operational emissions, about 40% of them still only reported operational emissions targets, and 25% reported no targets at all.

Footnotes

1. 'Nearly-deforestation free' is defined as companies that:

- have comprehensive zero deforestation commitments or policies;

- have a system to control, monitor and verify compliance across their supply chain; and

- report that more than 90% of their volumes are compliant.

All analysis is based on reported volumes. Claims have not been verified by CDP.

2. Source: World Resources Institute (2022) Forest Pulse: The Latest on the World’s Forests.

Further resources

-

Policy briefingAccelerating the Adoption of Landscape and Jurisdictional Approaches (Portuguese)Este policy brief chama a atenção para os desafios das leis ambientais internacionais, nacionais e subnacionais para desbloquear os benefícios das AP/AJs.

Policy briefingAccelerating the Adoption of Landscape and Jurisdictional Approaches (Portuguese)Este policy brief chama a atenção para os desafios das leis ambientais internacionais, nacionais e subnacionais para desbloquear os benefícios das AP/AJs. -

ReportGlobal Forests Report 2023 (Portugese)

ReportGlobal Forests Report 2023 (Portugese) -

ReportProtecting People and the Planet - Portuguese

- Load more