- New report finds capital goods sector is harnessing trends of electrification, digitization and automation to create a low carbon industrial revolution.

- 22 capital goods companies assessed, with Schneider Electric (France), Vestas (Denmark) and CNH Industrial (UK) identified as leaders.

- Companies such as Schneider Electric, Mitsubishi Electric (Japan), Siemens (Germany) and Honeywell (USA) lead the way on innovation, outperforming heavy industry peers with their high R&D spend and investment in transformative technologies.

- Demand for these transformative technologies are growing significantly. Energy storage systems could represent an investment opportunity worth US$103bn by 2030.

July 24, 2018, London: A low carbon industrial revolution is being driven by innovation in the capital goods sector – according to a new report ‘Bridging low carbon technologies’ from environmental non-profit and investment research provider CDP today. Capital goods companies provide the products and solutions that major high-emitting sectors such as power generation, buildings and transport rely on.

From microgrids to machine autonomy, energy storage to hybrid renewables, a set of 22 capital goods companies are assessed on how well they are harnessing trends such as electrification, digitization and automation to help meet the Paris Agreement commitment to keep global warming below 2°C.

The report analyzes companies in the ‘electrical equipment’, ‘industrial conglomerates’ and ‘heavy machinery’ parts of the sector, and highlights Schneider Electric, Vestas and CNH Industrial as leaders in their fields.

Highlights from the report include:

- Electrification is identified as the biggest opportunity for the capital goods sector, with microgrids and energy storage systems ranked as the technologies with the greatest potential for green economic transformation. The overall demand for energy storage is set to grow from current levels of 10 gigawatts to 125 GW by 2030, creating an investment opportunity of US$103bn1.

- Capital goods companies are identifying and investing in transformative and radical technologies such as microgrids, hybrid renewables and energy storage. Schneider, ABB, Mitsubishi Electric, Siemens and Honeywell lead the way on this.

- Mitsubishi Electric has also filed the largest number of high quality patents with 657 (per 10,000 employees) between 2000 and 2017. More than 60% of these focus on technologies that relate to automation, connectivity and digitalization.

- Renewable energy is an important profitability driver for several companies, with Vestas leading in hybrid renewables and large-scale digitalization.

- Heavy machinery lags electrical equipment and industrial conglomerates on innovation. Regulation of this sub-sector has so far focused on air quality rather than CO2 emissions and the end-markets served (e.g. agriculture, mining) are relatively traditional. At the same time, heavy goods vehicles are still largely dependent on diesel as a primary fuel.

- The main transition risk for the sector is managing emissions down the value chain. Scope 3 accounts for over 90% of sector emissions, however corporate disclosure and management of these emissions are poor. Less than a third of the companies we analyzed have a scope 3 emissions reduction target.

Carole Ferguson, Head of Investor Research, CDP said, “We are on the verge of a low carbon industrial revolution. Regulators and markets are demanding the decarbonization of high emitting sectors and the industrial corporations at the end of the chain are looking to their suppliers to find innovative new solutions and equipment. The good news is that the capital goods sector is starting to meet this challenge.”

“From hardware to software, decentralization to digitalization, industrial suppliers are finding solutions that build low carbon into the DNA of big industry. Energy storage is a great example of this - the rapid price decline for renewable power is driving an estimated twelve-fold increase in demand for energy storage, catalyzing even faster integration of renewable technologies for both centralised grids and distributed generation.”

“Despite the innovation demonstrated by many of these companies, it is disappointing to see that disclosure and management of emissions in the value chain are lagging. While these scope 3 emissions can be difficult to pinpoint, they are of huge importance to the capital goods sector given the wide markets these companies supply. Those companies that do not measure these emissions leave themselves exposed to risks and miss out on key opportunities from changing demands and regulation in the end markets they serve.”

The CDP report assesses companies across four key areas aligned with the recommendations from Mark Carney’s Task Force on Climate-related Financial Disclosures (TCFD). As the TCFD recommendations become mainstream, investors will increasingly expect capital goods companies to disclose how they are adjusting their business models to manage transition risks, while taking advantage of the opportunity to generate revenue from the global transition to a low-carbon economy.

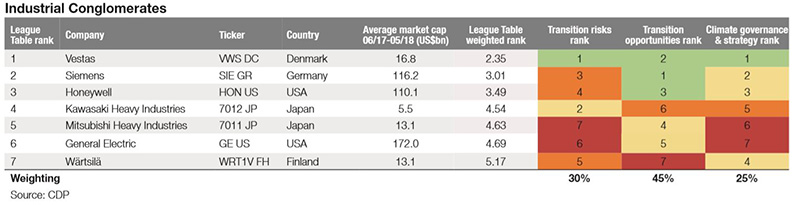

The rankings of the 22 companies assessed against the three sub-categories of ‘electrical equipment’, ‘industrial conglomerates’ and ‘heavy machinery’ are:

Ametek Inc. (electrical equipment), CK Hutchison Holdings Ltd (industrial conglomerates), CITIC Limited (industrial conglomerates), Caterpillar Inc. (heavy machinery), MAN SE (heavy machinery) did not respond to CDP’s 2017 climate change questionnaire and are therefore not included in this report. We encourage investors to raise this lack of transparency in discussions with company management.

You can view the executive summary of the report here.

- ENDS -

Notes to editor

For more information or for exclusive interviews with the CDP team, please contact:

- Caroline Barraclough, ESG Communications t: +44 (0)7503 771694 | e: [email protected]

- Rojin Kiadeh, CDP t: +44 (0) 203 818 3973 | e: [email protected]

- Tess Harris, CDP t: +44 (0) 203 818 3973 | e: [email protected]

Scope and methodology: Full details of the scope of the report and methodology used are included in the full version of the report. For the full report please contact [email protected]

About CDP and this report

About CDP

CDP is an international non-profit that drives companies and governments to reduce their greenhouse gas emissions, safeguard water resources and protect forests. Voted number one climate research provider by investors and working with institutional investors with assets of US$87 trillion, we leverage investor and buyer power to motivate companies to disclose and manage their environmental impacts. Over 6,300 companies with some 55% of global market capitalization disclosed environmental data through CDP in 2017. This is in addition to the over 500 cities and 100 states and regions who disclosed, making CDP’s platform one of the richest sources of information globally on how companies and governments are driving environmental change. CDP, formerly Carbon Disclosure Project, is a founding member of the We Mean Business Coalition. Please visit www.cdp.net or follow us @CDP to find out more.

The report

This research is part of a series of award winning in-depth sector analysis by CDP to provide investors with the most comprehensive environmental data analysis. It aims to identify the most material metrics for each specific sector and how they link to financial performance. Our methodology is unique as the weighting assigned to each metric is transparent and can be applied individually according to investor preferences. These rankings are not intended to identify definitive winners and losers for investment purposes, but rather to indicate strategic advantage in an industry where there is a significant regulatory impact on all major markets.

Reports on the oil & gas, steel, cement, automotive, electric utilities, chemicals and mining industries were released in 2015, 2016, 2017 and 2018.

1 Bloomberg New Energy Finance (BNEF)