New ‘Nerves of Steel’ report reveals how carbon pricing and stalled progress on decarbonization technologies will put steel industry through the mill.

- Steel industry accounts for 7% of global emissions and has made no progress to reduce emissions in a decade;

- Industry needs a technological transformation that will reduce its emissions per tonne of steel produced over 70% by 2050 in order to meet Paris Agreement objectives;

- 70% of steel industry will face a price on carbon by end of 2017, increasing risks for steelmakers that do not reduce their emissions;

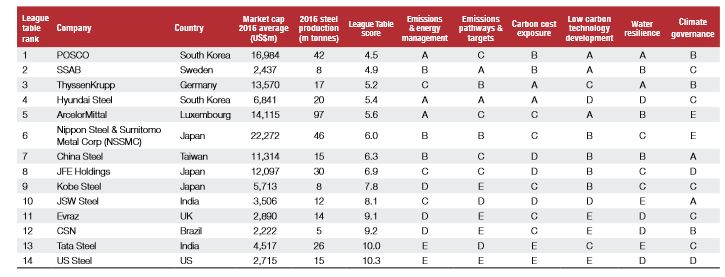

- POSCO, SSAB and Hyundai Steel are best performing companies on carbon-related metrics; Tata Steel and US Steel rank lowest of companies we were able to assess;

- China produces 50% of steel globally and will become subject to a carbon price in 2017, but of the 15 largest Chinese steelmakers, representing 40% of China’s steel produced, only one publicly discloses its greenhouse gas emissions;

October 6, 2016: A new report, analyzing a US$121bn grouping of the world’s largest steel companies, has found the industry needs to reduce its emissions by over 70% by 2050 in order to meet Paris Agreement objectives, but that progress on research and development (R&D) in emerging decarbonization technologies is limited and at early stages. With low industry profitability, R&D expenses have been cut by 14% in US$ terms in recent years and there are no commercially available technologies today which can achieve these targets. The threat to the industry is urgent as over 70% of world steel production will be subject to a carbon price by the end of 2017.

The report from CDP - voted no. 1 climate change research provider by institutional investors and winner of Investment Week’s Best SRI Research 2016 - reveals that there has been no industry-wide progress in improving emissions and energy efficiency levels in a decade with all emissions reduction targets set to expire by 2020. The report finds that the steel industry is responsible for 6-7% of global emissions, yet that of the 14 global steel companies analyzed, over 40% (six) have not published any emissions reduction targets beyond 2016.

Drew Fryer, Senior Analyst, Investor Research at CDP said:

“The steel industry will have to play a huge part in achieving the 2-degree scenario laid out in the Paris Agreement. However, there has been no progress in reducing its emissions over the past decade. Steelmakers need to prioritize funding of a technology transformation to reduce emissions in order to ensure targets are met. In particular, progress has been too slow to realize the potential of carbon capture and storage (CCS), with no pilot projects underway in the steel industry.”

Today’s report benchmarks leading steel companies on their management of climate issues finding South Korean firms POSCO and Hyundai Steel among the best performing, with Tata Steel and US Steel ranking lowest among those who disclose.

CDP’s summary League Table for steel companies shows:

Other findings from the report include:

- Over 70% of world steel production will be subject to a carbon price by end 2017, including from emissions trading schemes, carbon taxes or climate-focused coal taxes. Without success in realizing the potential of breakthrough low emissions technologies, steelmakers could face a continuously rising burden of carbon permit obligations;

- The industry’s progress in reducing emissions is inconsistent. More companies increased their emissions intensities than reduced them in the past seven years, with no industry-wide progress to improve energy efficiency in a decade;

- Only eight companies in the report have outlined emissions reduction targets. All those will expire by 2020. Six out of 14 companies in our sample have not published any forward looking targets, or have targets that expire in 2016;

- By 2030, 20% of sites assessed are projected to be in high water risk areas and 8% in extremely high risk areas. This could cause future business interruption exacerbated by climate change;

- China makes up 50% of global steelmaking production but is not providing investors with the carbon-related disclosures they require to assess individual company risk and preparedness, and make informed investment decisions;

- The steel industry is generally supportive of regulation but has obstructed it in practice, arguing it could create inconsistencies between regions with and without carbon prices. However, debate between industry and regulators over ‘carbon leakage’ could enter a new phase as more countries introduce carbon prices including China;

- Wuhan Iron and Steel, Nucor Corporation, Novolipetsk Steel OJSC, Steel Authority of India, Inner Mongolian Baotou Steel Union and SeverStal PAO which collectively represent over US$60 billion in market capitalization, did not respond to CDP’s 2016 climate change questionnaire and are therefore not included in this report. Investors should ask these companies why they are not providing transparency on their carbon emissions.

You can view the executive summary of the report here.

- ENDS -

Notes to editor

For more information or for exclusive interviews with the CDP team, please contact:

- Caroline Barraclough, ESG Communications t: 07503 771694 | e: [email protected]

- Rojin Kiadeh, CDP t : 07554430962 | e: [email protected]

Scope and methodology: Full details of the scope of the report and methodology used are included in the Executive Summary of the report [link].

About CDP and this report

About CDP

CDP, formerly Carbon Disclosure Project, is an international, not-for-profit organization providing the global system for companies, cities, states and regions to measure, disclose, manage and share vital environmental information. CDP, voted number one climate research provider by investors, works with 827 institutional investors with assets of US$100 trillion, to motivate companies to disclose their impacts on the environment and natural resources and take action to reduce them. More than 5,600 companies disclosed environmental information through CDP in 2015. CDP now holds the most comprehensive collection globally of primary corporate environmental data and puts these insights at the heart of strategic business, investment and policy decisions. Please visit www.cdp.net/ or follow us @CDP to find out more.

The report

This research is part of a series of award winning in-depth sector analysis by CDP to provide investors with the most comprehensive environmental data analysis. It aims to identify the most material metrics for each specific sector and how they link to financial performance. It is unique in that the weighting assigned to each metric is transparent and can be adjusted according to investor preference. Each of these metrics can provide a league in itself but the over-arching research reveals a League Table – combining all metrics. These rankings are not intended to identify definitive winners and losers for investment purposes, but rather to indicate strategic advantage in an industry where there is a significant regulatory impact on all major markets.

Reports on the cement, automotive, electric utilities and chemicals and mining industries were released in 2015.