New ‘In the pipeline’ report reveals European companies investing more in low-carbon technologies and shifting towards gas, as US companies risk being left behind

- Emissions footprint of oil and gas industry and its products account for approximately 50% of global CO2 emissions1;

- European majors outperform their US peers in the shift to gas, investments in low-carbon technologies and on wider climate governance and strategy;

- Current business models continue to rely heavily on finding and proving reserves. Traditional industry performance metrics (and their interpretations) potentially outdated with peak oil demand on horizon;

- Investors may be at risk as companies are currently only obligated to report proved reserves2, with limited insight into how sensitive estimates are to oil price volatility;

- Statoil, Eni and Total are best performing companies on carbon-related metrics relative to the peers; Suncor, ExxonMobil, and Chevron rank lowest of companies assessed.

November 22, 2016: A new report, analyzing a US$1.2tn3 grouping of the world’s major publicly-listed international oil and gas companies reveals a transatlantic divide as European companies outperform their US peers in preparedness for a low-carbon future by beginning to invest in alternative energy sources and shifting to gas.

The oil and gas industry, and the use of its products, accounts for approximately 50% of global CO2 emissions. Climate policies and disruptive technology affecting the use of hydrocarbon products in transport and utilities sectors will require the oil and gas industry to rapidly adapt in order to future proof their business.

The report from CDP – voted no. 1 climate change research provider by institutional investors– finds that the industry needs better capital discipline to secure its place in a low-carbon future through lowering its cost base or returning capital to shareholders. The research also reveals that the absence of robust data on probable and possible reserves is a significant loss of valuable information to investors looking to compare asset portfolio risk across companies.

Tarek Soliman, Senior Analyst, Investor Research at CDP said:

“On both sides of the Atlantic international oil and gas majors need to look at how they fit into an energy system which achieves the climate goals laid out in the Paris Agreement. Our research shows that European companies have been more active in developing transition strategies for the coming decade - which is expected to feature peak oil demand, and are starting to implement these. But more needs to be done across the board by oil and gas companies in exploring their future options, and investors will want to monitor this through more thorough and consistent disclosure.”

Meryam Omi, Head of Sustainability and Responsible Investment Strategy at LGIM, said:

“It is vital that the O&G sector aligns itself to the global goal of transitioning to a low carbon economy. There is an inevitable divergence in their commitments and transparency, which this report demonstrates. LGIM, will be using many of the findings to guide its overall engagement strategy with this sector."

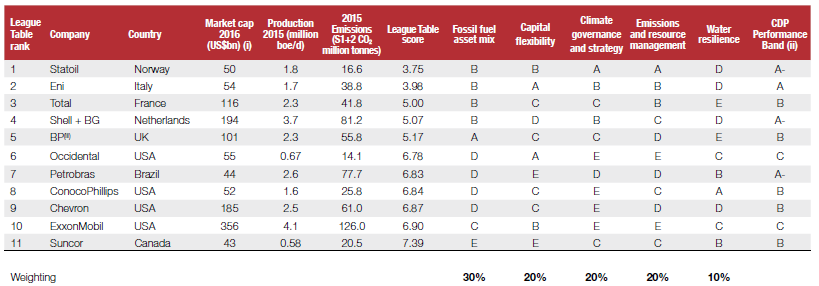

Today’s report benchmarks oil and gas company performance on climate issues and finds that Statoil, Eni and Total are the best performing companies on carbon-related metrics relative to peers, with Suncor, ExxonMobil and Chevron ranking lowest among those who disclose to CDP.

CDP’s summary League Table for oil and gas companies is below:

Other findings from the report include:

- Uncertain future: oil and gas majors face key short and long term decisions to secure their future business models, including improving capital discipline and rebalancing portfolios in the coming years and considering wider diversification or managed decline over the next decades.

- Regulation: the oil and gas industry will be impacted by regulatory action affecting demand in the downstream sectors which it supplies. This includes automobile fleet emissions for oil and emission reduction targets and carbon pricing for gas use in electricity generation.

- Operational efficiency: this remains an issue in the industry with the eleven companies in the study losing on average 6% of their natural gas production through flaring and methane venting and leakages. Resource management will affect demand for the industry’s products in their downstream use, for example the lifecycle carbon emissions gains of natural gas over coal in electricity generation can be eroded as a result of methane leakage (during extraction and transportation).

- Executive remuneration packages: these are currently heavily weighted to reward company performance on hydrocarbon production levels and reserve replacement indicators (only five companies currently have detailed climate-linked performance metrics).

- Water: 40% of onshore oil and gas upstream production is currently located in areas of medium or high water stress yet company disclosure remains behind other sectors facing similar risks.

- Saudi Aramco, Rosneft and PetroChina: which collectively represent over US$240bn in market capitalization4, did not respond to CDP’s 2016 climate change questionnaire and are therefore not included in this report. Investors should ask these companies why they are not providing transparency on their carbon risks.

Paul Simpson, CEO of CDP, said: "The oil and gas sector and its products contribute to approximately half of the world's CO2 emissions. This is an industry for investors to watch carefully in terms of climate risk and technology change. Mark Carney’s Taskforce on Climate related Financial Disclosure (TCFD) is expected to release its findings in December which will likely catalyze increased investor calls for full disclosures from oil and gas companies. There are reasons to be optimistic, some oil and gas majors have the balance sheets to transition to much lower carbon business models and play a key role in implementing the goals of the Paris Agreement."

You can view the executive summary of the report here.

### ENDS ###

Notes to editor

For more information or for exclusive interviews with the CDP team, please contact:

- Caroline Barraclough, ESG Communications t: 07503 771694 | e: [email protected]

- Rojin Kiadeh, CDP t: 07786626372 | e: [email protected]

Scope and methodology: Full details of the scope of the report and methodology used are included in the Executive Summary of the report [link]

About CDP and this report

About CDP

CDP, formerly Carbon Disclosure Project, is an international, not-for-profit organization providing the global system for companies, cities, states and regions to measure, disclose, manage and share vital information on their environmental performance. CDP, voted number one climate research provider by investors, works with 827 institutional investors with assets of US$100 trillion and 89 purchasing organizations with a combined annual spend of over US$2.7 trillion, to motivate companies to disclose their impacts on the environment and natural resources and take action to reduce them. More than 5,600 companies, representing close to 60% global market capitalization, disclosed environmental information through CDP in 2015. CDP now holds the most comprehensive collection globally of primary corporate environmental data and puts these insights at the heart of strategic business, investment and policy decisions. Please visit www.cdp.net/ or follow us @CDP to find out more.

The report

This research is part of a series of award winning in-depth sector analysis by CDP to provide investors with the most comprehensive environmental data analysis. It aims to identify the most material metrics for each specific sector and how they link to financial performance. It is unique in that the weighting assigned to each metric is transparent and can be adjusted according to investor preference. Each of these metrics can provide a league in itself but the over-arching research reveals a League Table – combining all metrics. These rankings are not intended to identify definitive winners and losers for investment purposes, but rather to indicate strategic advantage in an industry where there is a significant regulatory impact on all major markets.

Reports on the steel, cement, automotive, electric utilities and chemicals and mining industries were released in 2015 and 2016.

1 Based on IEA and EDGAR estimates, and accounting for estimated downstream Scope 3 emissions from use of sold products

2Companies disclose reserves in accordance with strict criteria outlined by SEC

3Based on 2015 average market capitalization

4 This figure applies to Rosneft and PetroChina as Saudi Aramco is not publicly listed.