While the world continues to reel from the impacts of the pandemic, it’s evident that more and more business leaders are joining the call to build forward a sustainable and resilient future.

Despite the many challenges in 2020, companies disclosing on TCFD-aligned reporting through CDP reached record numbers globally; This includes more than 3,000 companies from 21 markets across the Asia Pacific region (APAC), a nearly 20% increase from 2019 with many companies across China, India, and Southeast Asia (such as Malaysia, Thailand and Vietnam) having responded to CDP for the first time.

The region now accounts for nearly 30% of CDP’s global corporate responses, signalling a robust awareness across its key markets that are among the world’s fastest-growing economies.

Integrating climate issues into business strategy is now the norm

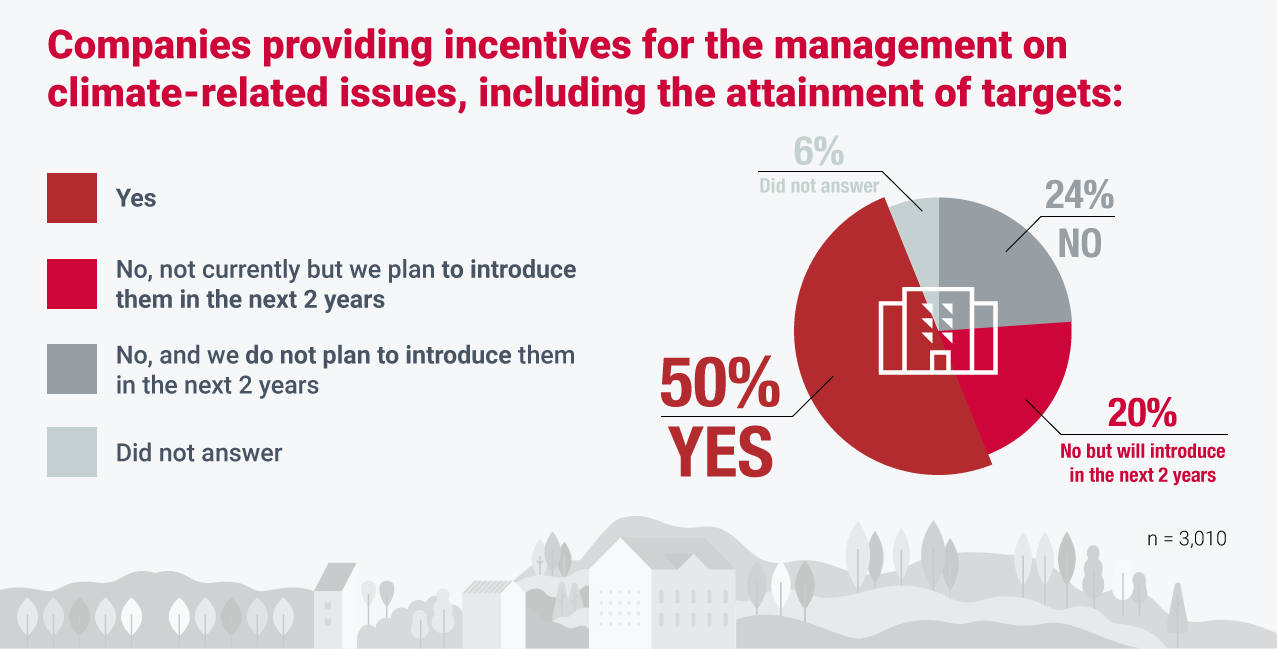

CDP’s APAC dataset of over 3,000 companies shows a majority of the disclosing companies now have board-level oversight on climate-related issues (79%) and have begun to integrate these issues into their business strategy.

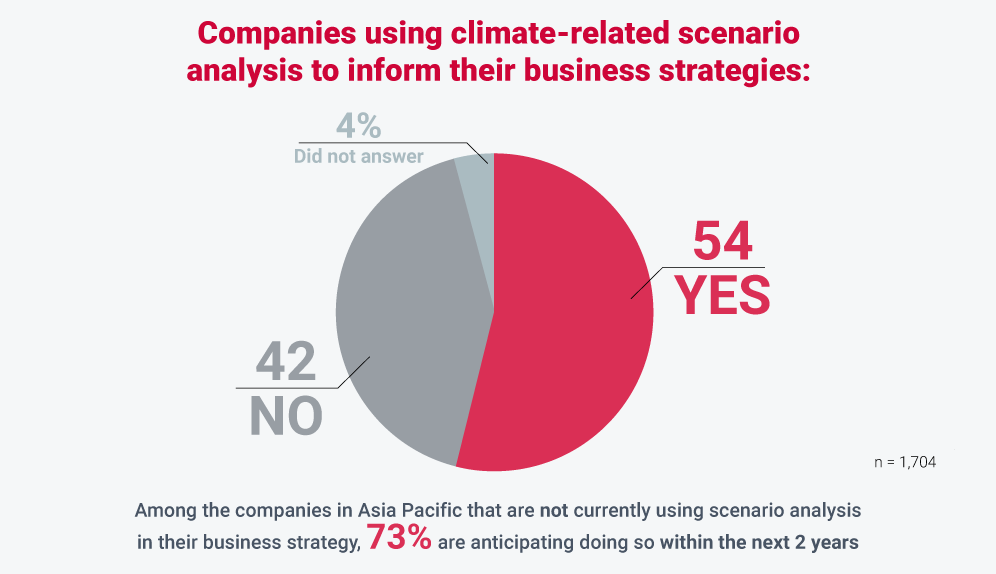

Of these, half have incentives in place for the management of climate issues. This includes setting and attaining climate targets and using climate-related scenario analysis to inform their business strategies.

TCFD-aligned reporting provides crucial direction on the governance and focus required on climate issues, empowering companies with better enterprise risk management practices to proactively address underlying risks posed by a changing climate.

Across the APAC region, CDP data shows nearly three out of four companies (74%) have identified climate risks that may have a substantive impact on their businesses. Of these, 60% are transition risks, most commonly related to policy and legal (31%) and market (15%), such as increased pricing of greenhouse gas (GHG) emissions, regulations on existing products and services, as well as enhanced emissions-reporting obligations.

Among physical risks, the most cited business risks are acute risks associated with increased severity of extreme weather events such as floods and cyclones (26%), attributed to the region’s pronounced vulnerability to disasters and climate risks.

The recently released Global Climate Risk Index 2021 finds that six out of ten countries most affected by climate change from 2000 to 2019 are in Asia.

…. But chronic and long-term climate risks remain underreported

Some companies have already started to manage such risks. For example, a developer from Southeast Asia reported introducing additional climate-resilient features, such as water-level sensors and water detention tanks, to their new and existing buildings located within high flood-prone areas to prevent property loss.

Companies are almost twice as likely to consider acute physical risks when compared to chronic physical risks such as rising temperature and sea-level rise.

At the same time, our data suggests that chronic physical risks are relatively underreported (only 12% of all risks identified), indicating a potential lack of corporate awareness and action to address risks that may affect their business over a longer time horizon.

McKinsey Global Institute estimates that the impact on labour productivity from chronic increases in heat and humidity levels alone could cost Asia up to US$4.7 trillion of annual GDP by 2050. This accounts for more than two-thirds of the total annual global GDP impact, and about US$1.2 trillion in capital stock in Asia could be lost to riverine flooding per year by 2050.

Increased reporting on direct operations, but emissions data from supply chains remains elusive

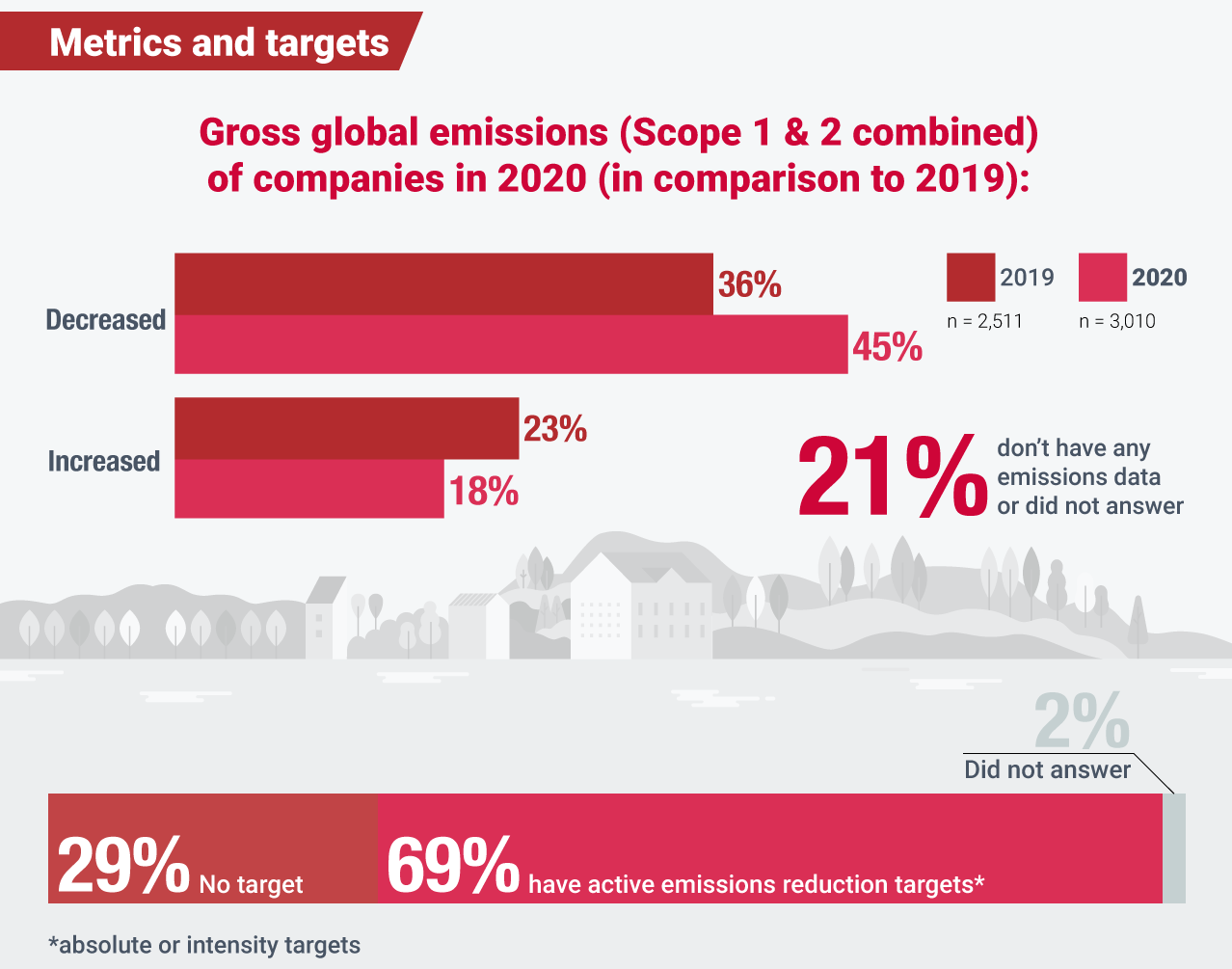

Approximately 70% of APAC companies disclosing through CDP have emissions targets (including absolute or intensity targets) and are putting in place emissions reduction initiatives, such as allocating a dedicated budget for energy efficiency, low-carbon product and R&D, or setting an internal price on carbon.

As a result of such initiatives, 45% of the APAC disclosing companies reported a year-on-year decrease in direct (Scope 1 and 2) emissions in 2020.

The emission reduction performance however varies significantly by sector. We find, for instance, more APAC companies in the apparel industry disclosed on their gross Scope 1 and 2 emissions – a 28% spike when compared to last year, indicating that assessment of emissions and target setting is becoming the norm in certain sectors.

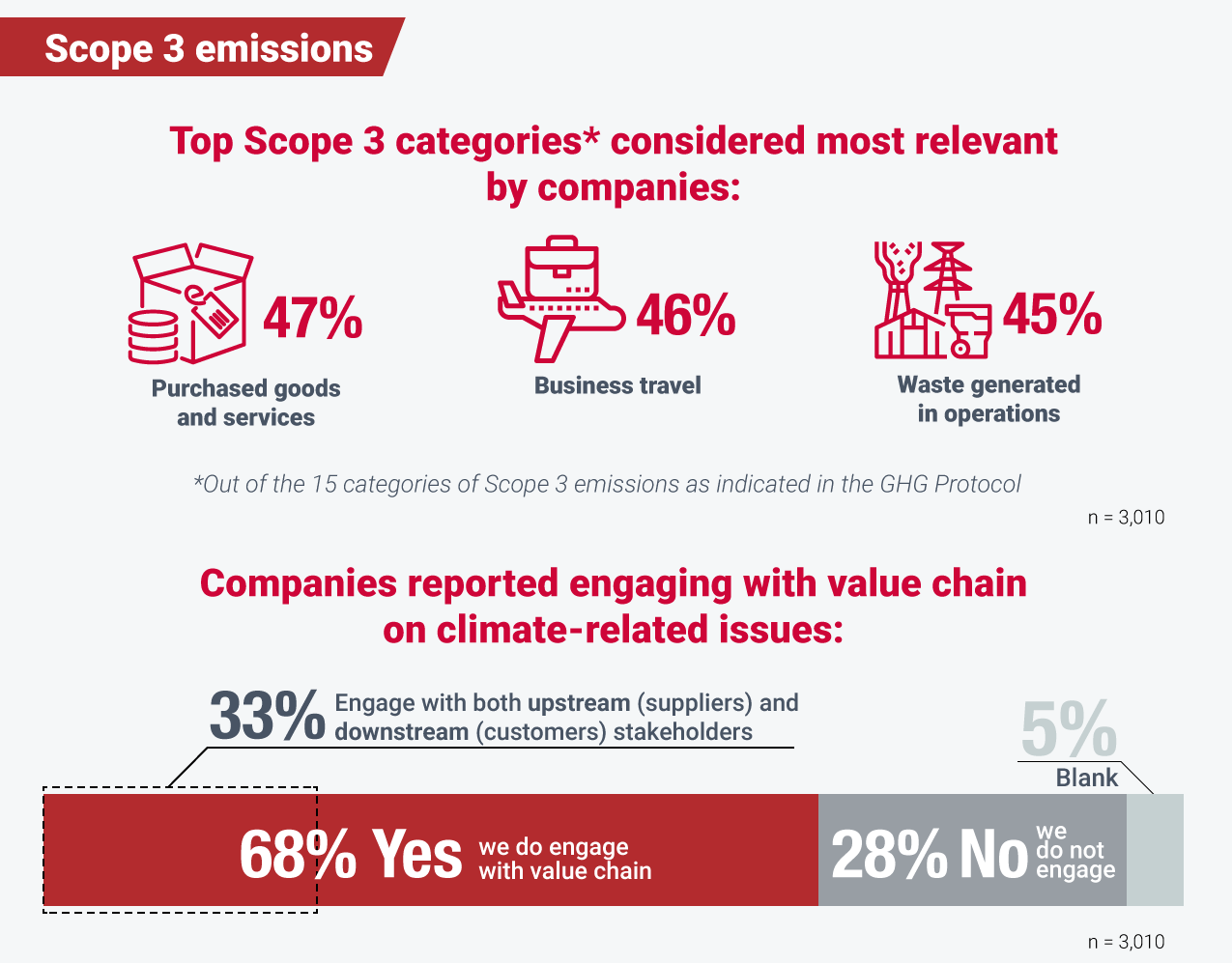

While this is encouraging, a key area that APAC companies need to focus on is engaging with their supply chains on climate-related risks and opportunities.

CDP’s data shows that only 25% of the region’s disclosing companies include all stages of their value chain when performing risk assessments. Approximately 30% of companies neither engage with their upstream nor downstream stakeholders.

Momentum mounts for climate action in the supply chain

As indicated in CDP’s 2020 supply chain report, supply chain emissions are on average 11.4 times as high as a company’s operational emissions. This makes multi-stakeholder engagement across the value chains critical in achieving global net-zero goals.

This is of particular relevance to the manufacturing sector which accounts for approximately 60% of all responding companies in APAC.

Despite the sector’s heightened exposure to supply chain risks, our data shows that less than 20% of manufacturing companies have established risk management processes that cover all stages of their value chain, with more than half of the companies considering only direct operations in their risk assessment.

This suggests the manufacturing sector is underestimating climate risks in upstream and downstream assessments, rendering the business operations of these companies more vulnerable to supply chain disruptions.

Potential financial impacts from regulatory or market changes are also of key relevance to the manufacturing sector.

For instance, several companies reported to CDP this year that they are anticipating the European Union (EU)’s tightening of eco-design requirements for servers and data storage products by 2030. Electronics suppliers in APAC whose customers are from the EU have identified this as a transition risk within downstream operations.

Given climate-related financial risks within supply chains, the challenge is for corporate leaders in the region to raise their climate ambitions and collaborate to reduce their emissions throughout their value chain.

A key action that CDP recommends is for corporates to develop and validate targets through the Science Based Targets initiative (SBTi).

Through SBTi’s process, companies are required to set targets for Scope 3 if their Scope 3 emissions are 40% or more of their total emissions. APAC companies are starting to address upstream risks by setting supplier engagement targets.

Companies are also increasingly using CDP’s supply chain program to request data from their suppliers, use the data in supplier engagement, measure and manage their Scope 3 emissions and track progress towards their science-based targets.

For example, since becoming CDP’s first Supply Chain Program member in Australia, the telecommunications and technology company Telstra has 89% of its top-100 suppliers reporting their environmental impacts through CDP, which is well above the global average disclosure rate.

Setting science-based targets is the critical first step towards decarbonisation

Encouragingly, there are signs that companies in APAC are increasingly looking to seize the business opportunities arising from the transition to a zero-carbon economy.

68% of APAC companies disclosing through CDP are now aware of the financial or strategic value of climate assessments as they identify opportunities ranging from developing new products and services (44%), improving resource efficiency (22%), to identifying new energy sources (17%).

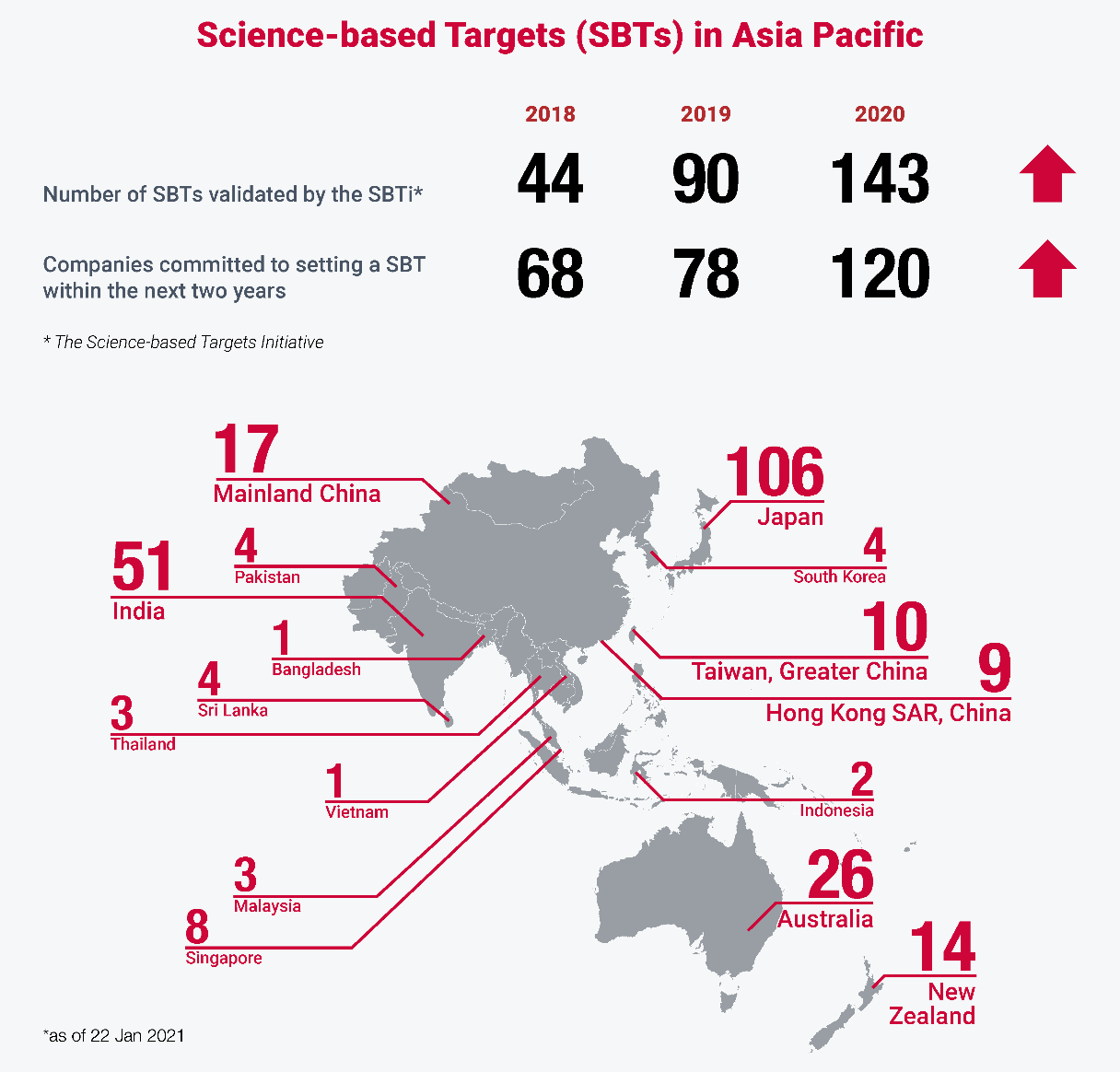

Across the region, we are also seeing companies committing to targets approved by the Science Based Targets initiative (SBTi). The region now accounts for more than 260 science-based targets, a 57% increase when compared to 2019. Notably, 48 of these companies are also aligning their science-based targets with a 1.5 °C pathway, leading the world’s effort in meeting the Paris Agreement goals aiming to mitigate the worst impacts of climate change.

Apart from setting mid- and long-term targets in line with keeping warming to 1.5°C, companies should also look at other ways in which they can help address interconnected issues concerning climate adaptation and systemic resilience, for example through innovative approaches to climate finance, investing in nature-based solutions, and strengthened cooperative action.

As we embark on a new decade toward our goals to meet the Paris Agreement, it is paramount that companies and financial institutions continue to roll out and expand long-term decarbonisation strategies and green finance initiatives that will help achieve a net-zero future.

CDP will continue to support businesses across regions in their journey towards climate resilience through increased transparency, disclosure and setting ambitious targets in line with the latest climate science.